A charitable remainder trust (CRT) is an irrevocable trust that generates a potential income stream for you, as the donor to the CRT, or other beneficiaries, with the remainder of the donated assets going to a charity like TFH.

This charitable giving strategy generates income and can enable you to pursue your philanthropic goals while also helping provide for living expenses. Charitable trusts can offer flexibility and some control over your intended charitable beneficiaries as well as lifetime income, thereby helping with retirement, estate planning and tax management.

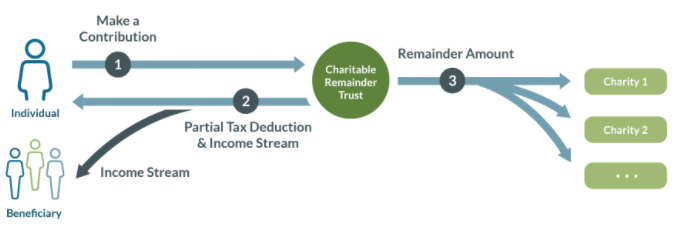

How a charitable remainder trust works

A charitable remainder trust is a “split interest” giving vehicle that allows you to make contributions to the trust and be eligible for a partial tax deduction, based on the CRT’s assets that will pass to charitable beneficiaries. You can name yourself or someone else to receive a potential income stream for a term of years, no more than 20, or for the life of one or more non-charitable beneficiaries, and then name one or more charities to receive the remainder of the donated assets.

There are two main types of charitable remainder trusts:

- Charitable remainder annuity trusts (CRATs) distribute a fixed annuity amount each year, and additional contributions are not allowed.

- Charitable remainder unitrusts (CRUTs) distribute a fixed percentage based on the balance of the trust assets (revalued annually), and additional contributions can be made.

Contributions to CRATs and CRUTs are an irrevocable transfer of cash or property and both are required to distribute a portion of income or principal, to either the donor or another beneficiary. At the end of the specified lifetime or term for the income interest, the remaining trust assets are distributed to one or more charitable remainder beneficiaries.

NOTE – THF does not have the capacity to create or set up a CRT, the individual donor will need to do this with an attorney, not a tax advisor or financial planner.

- 1. Make a partially tax-deductible donation

Donate cash, stocks or non-publicly traded assets such as real estate, private business interests and private company stock and become eligible to take a partial tax deduction. The partial income tax deduction is based on the type of trust, the term of the trust, the projected income payments, and IRS interest rates that assume a certain rate of growth of trust assets. - 2. You or your chosen beneficiaries receive an income stream

Based on how you set up the trust, you or your stated beneficiaries can receive income annually, semi-annually, quarterly or monthly. Per the IRS, the annual annuity must be at least 5% but no more than 50% of the trust’s assets. - 3. After the specified timespan or the death of the last income beneficiary, the remaining CRT assets are distributed to the designated charitable beneficiaries.

When the CRT terminates, the remaining CRT assets are distributed to the charitable beneficiary, which can be public charities or private foundations. Depending on how the CRT is established, the trustee may have the power to change the CRT’s charitable beneficiary during the lifetime of the trust.

Is a charitable remainder trust right for me?

The CRT is a good option if you want an immediate charitable deduction, but also have a need for an income stream to yourself or another person. It is also a good option if you want to establish one by will to provide for heirs, with the remainder going to a charity like THF.

Note – None of this information should be construed as legal or tax advice. In making a charitable gift, it is always important to seek the advice of your attorney or tax advisor.

If you establish a Charitable Remainder Trust to benefit THF, please contact our Planned Giving Director, Michael Kunkel, to let us know so we can thank you and welcome you into our Legacy Society. Notifying us will enable us to plan for the use of your future gift.

Our Federal Tax ID# is 20-1419753.